Growing a business takes more than ideas—it takes capital. Long term business loans provide reliable financing that helps companies expand, invest, and scale without crushing short-term repayment pressure. Whether you’re purchasing equipment, acquiring property, or funding strategic growth, the right long-term loan can transform your business trajectory.

In this guide, we break down how long term business loans work, who they’re best for, how to qualify, and how to choose the smartest option—based on real-world lending experience and modern financing standards.

What Are Long Term Business Loans?

Long term business loans are financing products designed to be repaid over an extended period—typically 3 to 25 years—with fixed or predictable monthly payments.

Unlike short-term loans that focus on quick cash flow fixes, long-term loans are built for sustainable growth and long-term investments.

Key Characteristics

-

Repayment terms: 3–25 years

-

Lower monthly payments than short-term loans

-

Fixed or variable interest rates

-

Often require strong credit and business history

-

Suitable for major business investments

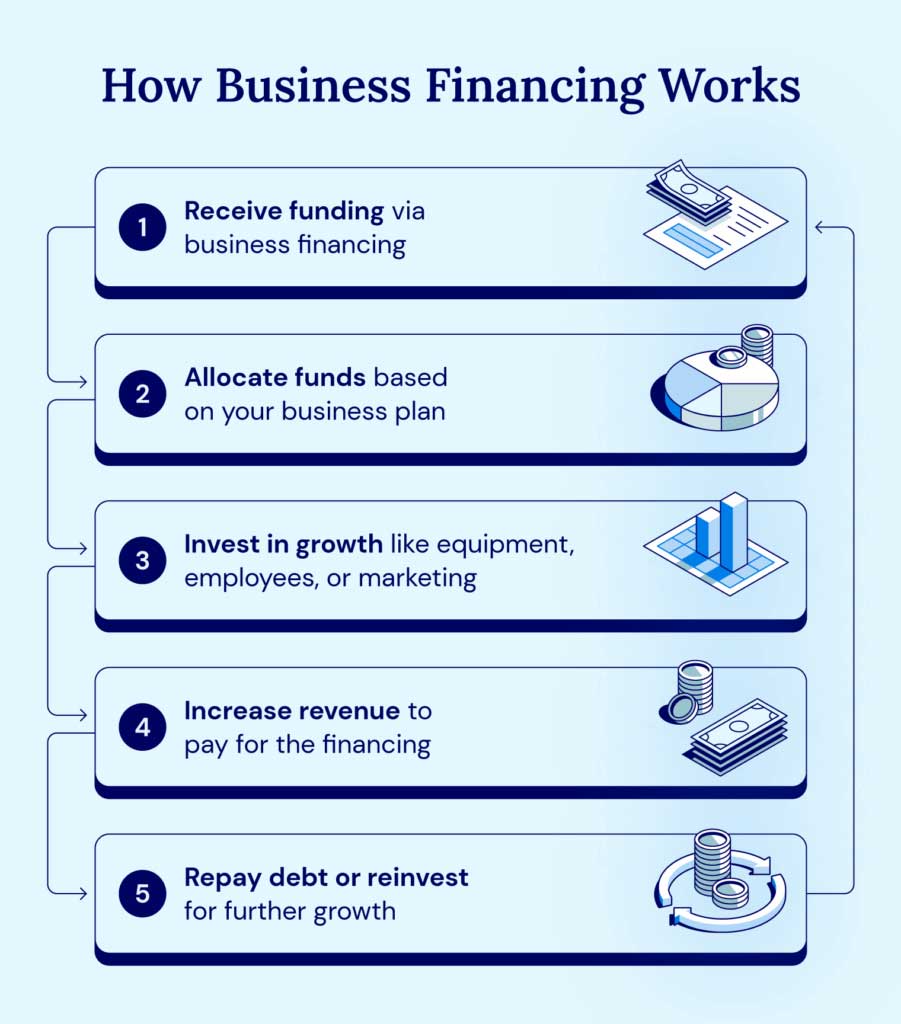

How Long Term Business Loans Work

When you take out a long-term loan, you receive a lump sum upfront and repay it in scheduled installments over time.

Typical Loan Structure

-

Application & underwriting

-

Loan approval and funding

-

Monthly repayment schedule

-

Interest paid over the life of the loan

Because lenders take on more risk over longer periods, they carefully evaluate:

-

Business revenue

-

Credit history

-

Debt-to-income ratio

-

Business stability and cash flow

Types of Long Term Business Loans

Understanding your options helps you choose the most cost-effective financing.

1. Traditional Bank Term Loans

Best for established businesses with strong financials.

Pros

-

Lowest interest rates

-

Long repayment terms

-

Predictable payments

Cons

-

Strict qualification requirements

-

Slower approval process

2. SBA Long Term Business Loans

Government-backed loans offering flexible terms.

Common SBA programs

-

SBA 7(a) loans

-

SBA 504 loans

Why businesses choose SBA loans

-

Lower down payments

-

Longer terms (up to 25 years)

-

Competitive interest rates

3. Online Long Term Business Loans

Ideal for businesses needing faster approval with moderate credit.

Advantages

-

Faster funding

-

Easier qualification

-

Digital application process

Trade-offs

-

Higher interest rates than banks

-

Slightly shorter terms than SBA loans

4. Commercial Real Estate Loans

Designed for purchasing or refinancing business property.

Use cases

-

Office buildings

-

Warehouses

-

Retail spaces

These loans often come with the longest repayment terms available.

What Can Long Term Business Loans Be Used For?

Long-term financing supports strategic business goals rather than emergency expenses.

Common Uses

-

Business expansion

-

Purchasing real estate

-

Equipment financing

-

Acquisitions and mergers

-

Debt consolidation

-

Franchise investments

Using long term business loans for revenue-generating activities improves ROI and lender confidence.

Long Term vs Short Term Business Loans

| Feature | Long Term Loans | Short Term Loans |

|---|---|---|

| Repayment period | 3–25 years | 3–24 months |

| Monthly payments | Lower | Higher |

| Interest rates | Lower overall | Higher |

| Best for | Growth & assets | Cash flow gaps |

| Approval speed | Moderate | Fast |

Rule of thumb:

If the investment benefits your business for years, long-term financing makes more sense.

Interest Rates and Costs Explained

The total cost of long term business loans depends on multiple factors.

Typical Interest Rate Ranges

-

Bank loans: 5%–9%

-

SBA loans: 6%–10%

-

Online lenders: 8%–20%

Additional Costs to Consider

-

Origination fees

-

Closing costs

-

Prepayment penalties

-

Collateral requirements

Always evaluate APR, not just the interest rate.

Qualification Requirements for Long Term Business Loans

Lenders prioritize stability and repayment ability.

Common Requirements

-

Time in business: 2+ years

-

Annual revenue: $100,000+

-

Credit score: 650+ (higher for banks)

-

Positive cash flow

-

Business plan or financial projections

Strong documentation increases approval odds and lowers interest rates.

How to Improve Your Approval Chances

Even if you don’t qualify today, you can prepare.

Actionable Steps

-

Improve business and personal credit scores

-

Reduce outstanding high-interest debt

-

Maintain consistent revenue

-

Prepare accurate financial statements

-

Build relationships with lenders

Expert borrowers plan financing months in advance, not when cash is urgent.

Pros and Cons of Long Term Business Loans

Advantages

-

Predictable monthly payments

-

Lower payment pressure

-

Better for large investments

-

Improves long-term planning

-

Can boost business credit profile

Disadvantages

-

Longer approval process

-

More documentation required

-

Total interest paid may be higher over time

-

Often requires collateral

When Long Term Business Loans Make the Most Sense

Long-term financing isn’t for every situation.

Best Scenarios

-

Scaling operations

-

Buying property or equipment

-

Expanding into new markets

-

Refinancing expensive debt

-

Stabilizing long-term cash flow

If your business goal extends beyond one year, long-term funding aligns better.

How to Choose the Right Long Term Business Loan

Not all loans are equal—even with similar rates.

Smart Comparison Checklist

-

Total repayment cost

-

Term length flexibility

-

Prepayment penalties

-

Collateral requirements

-

Funding speed

-

Lender reputation

Always compare at least 3 lenders before deciding.

Long Term Business Loans and E-E-A-T Considerations

Search engines reward content backed by expertise and trust.

Why This Matters for Borrowers

-

Reputable lenders offer transparent terms

-

Trusted advice reduces financial risk

-

Experience-based guidance leads to smarter decisions

Businesses that approach financing strategically outperform those that borrow reactively.

Common Mistakes to Avoid

Avoid these costly errors when applying.

Top Pitfalls

-

Borrowing more than needed

-

Ignoring total loan cost

-

Overlooking repayment flexibility

-

Applying without improving credit

-

Choosing speed over sustainability

A loan should support growth—not restrict it.

FAQs About Long Term Business Loans

How long is a long term business loan?

Typically between 3 and 25 years, depending on lender and loan type.

Are long term business loans hard to get?

They require stronger financials, but preparation greatly improves approval odds.

Do long term business loans require collateral?

Often yes—especially for banks and SBA loans—but some online lenders offer unsecured options.

Can startups get long term business loans?

Most lenders prefer established businesses, but SBA programs may allow newer companies with strong plans.

Final Thoughts: Are Long Term Business Loans Worth It?

For businesses focused on sustainable growth, long term business loans remain one of the smartest financing tools available. They provide stability, predictability, and the financial breathing room needed to scale confidently.

When chosen carefully and used strategically, long-term financing isn’t just debt—it’s a growth engine.

Want More Smart Business Financing Guides?

Explore expert-backed insights and funding strategies at LoadingTips.com—where smarter money decisions begin.

Internal Link Suggestions

- Online Mortgage Lenders Explained: How to Compare Rates, Get Approved Faster, and Save Thousands

- Online Business Loan: A Step-by-Step Guide to Get Fast, Flexible Funding in 2026

- Business Car Insurance Quote: How to Get the Best Coverage at the Lowest Cost in 2026